Social Agriculture Reports

Table of Contents

- Defining Social Agriculture

- Research Context

- Literature Review Methodology

- Primary Research Question

- Executive Summary & Key Findings

- Kenyan Agriculture at a Glance

- ICT for Agriculture

- Mobile Agriculture

- The Rise of Internet-enabled Devices and Services

- Digital Agriculture

- Scaling and sustainability in Digital Agriculture

- Social platforms for Agricultural Extension

- Social Agriculture

- Social platforms value proposition in Agriculture

- Case Study – Facebook

- Case Study – WhatsApp

- Demographics of Social Agriculture users

- Youth in Social Agriculture

- Social Commerce in Social Agriculture

- Expression of user needs via social agriculture

- Social and Critical Theory for Social Agriculture

This report is part of an overall research study on social agriculture in Kenya and will be followed by research in Ghana and Nigeria.

Acknowledgements

This literature review was written by Finn Richardson from Kilimo Source, with guidance from Jonathan Donner at Caribou Digital. Special thanks to Adam Wills, Catherine Kamanu, Emrys Schoemaker, and Eoghan McDonaugh. Special thanks to Robyn Read at the Mastercard Foundation for support and enthusiasm throughout the process.

For questions about this literature review, please contact Finn Richardson at fpk.richardson@gmail.com or Jonathan Donner at jonathan@cariboudigital.net.

For questions about the social agriculture research, please contact Emrys Schoemaker at emrys@cariboudigital.com.

This report is the joint effort of the authors and research partners Learn.Ink, Habitus Insight, and Caribou Digital, in partnership with the Mastercard Foundation. The views presented in this paper are those of the authors and do not necessarily represent the views of the Mastercard Foundation.

Recommended Citation

Kilimo Source and Caribou Digital. Social Agriculture: A Literature Review. Farnham, Surrey, United Kingdom: Caribou Digital Publishing, April 2022. www.platformlivelihoods.com/social-agriculture- lit-review/.

Defining Social Agriculture

Caribou Digital is observing a significant scale of activity on social media platforms by farmers and others working in agriculture around the world, specifically in countries with a high proportion of their workforce in agriculture. We term this phenomenon social agriculture and define it in the following way:

Social agriculture refers to a set of practices that support agricultural livelihoods—including information exchange, support mechanisms, and markets—where these are based on the use of social media platforms in countries with a high proportion of their workforce in agriculture.

Three key aspects of social agriculture

Agriculture Information Exchange

The process of requesting, gathering, analyzing, and disseminating information about prices, best practices, and other topics relevant to agriculture practitioners.

Agricultural Support Mechanisms

Organizations or groups that support each other as agricultural practitioners through a combination of peer-to-peer camaraderie, collective action as well as financial or in-kind support.

Agricultural Markets

Places where buyers and sellers can meet to facilitate the exchange or transaction of goods and services relating to agriculture.

With an outline of the concept of social agriculture in view, the following points illustrate important aspects of our understanding of this phenomenon.

- We stress the term livelihoods insofar as it comprises the capabilities, material and social resources, and activities required for a person working in agriculture. Livelihoods is a concept broader than only the way social media supports commercial interactions within the agriculture sector.

- We are using a broad sense of social media as a set of digital platforms that allows users to create and exchange information, ideas, interests, and other forms of expression via virtual communities and networks. This covers services like Facebook, WhatsApp, YouTube, Instagram, TikTok, and more.

- We stress that many of the interesting practices described here unintentionally arise from the infrastructure and logic of social media platforms themselves. In other words, individuals working in agriculture often repurpose existing platform features to try to achieve the intended “ends” of social agriculture, i.e., information exchange, buying and/or selling, etc.

- We often see the reinforcement of social capital as integral to the phenomenon of social agriculture. In other words, some of the early beneficiaries of the system (e.g., those receiving information) must later become benefactors (e.g., become information providers) for the many of these systems to work. In particular, information exchange and support mechanisms depend upon the culture of reciprocity between individuals in the social agriculture space.

Research context

This literature review was conducted to support a research project on Social Agriculture (defined at the opening of this document) conducted in partnership with MasterCard Foundation and in collaboration between Caribou Digital (UK), Kilimo Source (Kenya), Learn.Ink (UK), and Habitus Insight (UK). This literature review seeks to:

- Identify the extent to which the phenomenon defined as social agriculture has already been documented in the literature.

- Position the definition and research within the literature by drawing upon literature from relevant, intersecting, and complementary fields, including Smallholder Agriculture, Digital Agriculture, Social Media, and Social Commerce.

- Understand the affordances granted by social media for the pursuit of agricultural livelihoods and the ways in which these are being applied by rural agriculturalists.

The research locus is Kenya, though social agriculture is very much a global phenomenon. Thus there is global literature that is relevant and broadly applicable in terms of theory, practice, and context-framing, which has been included where relevant. Quantitative analysis of the Social Agriculture Ecosystem was also conducted to complement this literature review and support the broader research agenda.

Literature review methodology

Primary searches were conducted using Google Scholar with different combinations of the search terms: Social Agriculture, Social Media, Agriculture, Africa, Social Commerce, Facebook, WhatsApp. The first 200 results for each search were scanned for relevance, and further publications were sourced through professional networks. This literature review synthesizes all relevant publications. Wherever possible, peer-reviewed literature have been included and are cited and referenced in black. Due to the highly contemporary nature of the field of study, and the fast pace of progress within the sector, practitioner literature sources including industry and agency reports, unpublished research theses, news articles, and blogs are also included where relevant (cited and referenced in gray.)

Researchers have used the term social agriculture in semantically different contexts, almost always referring to community development and social inclusion in agriculture, in ways that have little to do with digital technologies. Rhoades & Aue (2010) use the phrase social agriculture in the title of a USA-based study among agricultural broadcasters. In the context and definition proposed in this study, the term social agriculture is notably absent from the literature. However we can infer the occurrence of our definition of social agriculture when the research and discussion intersects social platforms with agricultural livelihoods in countries with a high proportion of their workforce in agriculture.

Primary research question

How widespread is social agriculture, and what are the opportunities to strengthen platform practices to deliver better outcomes for farmers?

Subquestions:

- How many farmers (in what sectors) in each country are involved in social agriculture? Of those, what proportion actually buy and sell?

- How do farmers use social media throughout the agricultural supply chain/business journey?

- What are the largest venues or platforms for social agriculture?

- Is social agriculture more or less productive than alternative digital agriculture platforms?

- Are there limits to social agriculture, for example, innovation cul-de-sacs or limits to scale?

- What kinds of farmers engage in social agriculture and with what degree of success (gender, youth, education, resources, location)?

- Are there barriers to entry, and how do they intersect with dynamics of inclusion and exclusion, including gender?

- What platform practices help farmers succeed in social agriculture?

- How do platform affordances shape farming practices, and what are the implications for farmers’ success in social agriculture?

- What improvements (in training, functionality, value added services (VAS)/related businesses) can increase the effectiveness of social agriculture?

- What are the opportunities to strengthen practices that lead to better outcomes for farmers?

Executive summary and key findings

- Social platform use for agricultural livelihoods has achieved far greater scale and adoption than most purpose-built mobile/digital agriculture platforms, which have typically struggled to reach scale and commercial sustainability for a wide range of reasons, including contextual constraints, design challenges, and issues with deployment.

- By comparison to many digital agriculture platforms, social platforms are widely known, familiar, free to use, and have a broad range of functionalities which enhance adoption.

- Social platforms offer a far richer user experience, broader networking capacities, and higher level of interactivity than most purpose-built digital agriculture platforms.

- Internet-enabled device ownership, which enables access to social platforms, is on the rise and opening up opportunities for many users, including rural agriculturalists.

- Social platform affordances enable many of the same value propositions and use-cases that digital agriculture platforms target, including the improvement of information pathways, market efficiencies, empowerment of individuals and communities, audience engagement and networking, and rich media learning experiences.

- Social platforms are revolutionizing agricultural extension activities, though institutions are lagging behind the general public in terms of adoption and interactive use of platforms.

- Facebook and WhatsApp are by far the most widely used platforms for social agriculture, and user-generated groups are key to the value of social platforms for social agriculture.

- Social platforms are popular sources of agricultural information and market-making, but there’s more to the picture, including communication, relational work, collaboration, cross-learning and innovation, peer-to-peer support, and the generation of social capital.

- Agricultural buying and selling patterns have been increasingly moving towards social platforms, far outpacing the level of activity on existing digital agriculture marketplaces.

- Social agriculture broadly reflects existing digital divides and gendered accessibility constraints; users are more likely to be younger, wealthier, more male, and more highly educated than the general population.

- Depictions of agriculture on social platforms are encouraging youth participation with agriculture, changing perceptions and reversing a historical trend for the abandonment of agricultural livelihoods by younger generations.

- Informal social commerce (practiced via social platforms) is on the rise, particularly in emerging markets where formal e-commerce alternatives are scarce, and/or where fewer people are sufficiently financially integrated to engage in formal e-commerce.

- A range of social platform affordances have been appropriated in complex and nuanced ways for the practice of informal social commerce. An array of structures, norms, and practices are employed to overcome limitations, to build trust, and to generate social capital.

- Informal social commerce is particularly popular among women entrepreneurs—who are vastly overrepresented in the space—particularly in contexts where they face systemic and normative constraints to establishing business enterprises.

- Platform developers are racing to implement integrated payment functionalities to enhance user trading experiences and capitalize on the huge amount of commerce occurring on social platforms.

- Diffusion and appropriation of social platforms and their affordances for agricultural livelihoods are likely to widen and become increasingly complex and nuanced.

- Social platforms are open-access, capacity-building tools by which users actively, organically, intuitively, and iteratively express and meet their needs.

Kenyan Agriculture at a Glance

Kenya’s prosperity and development are still highly dependent on its agricultural sector, which is one of the main drivers of the country’s economic growth (Henze & Ulrichs, 2016; Wangu, 2014). The sector directly contributes 26% of the country’s GDP and another 27% indirectly through linkages with other sectors (FAO, 2021). Approximately 45% of government revenue is derived from agriculture (Wangu, 2014); the sector accounts for 65% of export earnings (FAO, 2021) and over 75% of industrial raw materials (Wangu, 2014).

The agricultural sector directly employs more than 40% of the total population (FAO, 2021), more than 50% of the employed population (D’Alessandro et al., 2015), and more than 70% of the rural population (FAO, 2021; Henze and Ulrichs, 2016). Kenya’s domestic agriculturalists produce 63% of the food consumed in the country (Rapsomanikis, 2015), and agriculture provides livelihoods (employment, income, food security needs) for more than 80% of the Kenyan population (FAO, 2021).

Kenya’s agricultural sector is mainly composed of rural smallholder farmers who practice rain-fed agriculture on less than three hectares of land (D’Alessandro et al., 2015). Sixty-nine percent of these farmers are middle-aged (36–64 years of age) and 11% are elderly (65+). Only 20% are “youth” (18–35 years of age). A greater proportion of those employed in agriculture are women (59.3%) compared to men (49.5%) (World Bank, 2020).

Kenya’s rural smallholder farmers are typically characterized by limited access to land, low skills and family labor, rainfall-dependent subsistence farming practices based on rudimentary inputs, and ultimately low bargaining power (Misaki et al., 2018). On-farm productivity is often low, typically linked to low adoption of improved agricultural technologies and inputs and driven by a mix of factors, including limited access to education, information, capital, and inputs, as well as individual perception and risk preferences (Aker, 2011). This dynamic can trap smallholder rural farmers, who may have few alternative sources of employment and income, in a cycle of poverty (Henze & Ulrichs, 2016).

Nevertheless rural smallholder farmers produce a remarkable 75% of Kenya’s agricultural output (D’Alessandro et al., 2015). Given the importance of the agricultural sector in the Kenyan economy and the significant proportion of the population—particularly among the rural poor—directly and indirectly involved in the agricultural value chain, growth in this sector is therefore likely to have a greater impact on a larger section of the population than any other sector (FAO, 2021; Wangu, 2014). Historically, this is the case; Kenyan agriculture has contributed more proportionately to GDP growth than other sectors (Alila & Atieno, 2006).

Smallholder livelihoods are becoming increasingly diverse (Adelaja, 2021). The agricultural sector is becoming increasingly knowledge intensive (Adejo and Opeyemi, 2019), and farmers require more information to make increasingly complex decisions (FAO, 2015). As a result, farmers’ access to reliable, timely, and locally relevant information, including agricultural practices, input use, accurate local weather predictions, and real-time prices and market information (Emeana, Trenchard, & Dehnen-Schmutz, 2020) is increasingly critical to their competitiveness (Adejo & Opeyemi, 2019).

Historically, such information dissemination has been delivered by agricultural extension departments and field agents (Henze & Ulrichs, 2016; Wangu, 2014). However, the number of extension workers in Kenya has decreased dramatically in recent decades (Kioko, 2016), while the number of small scale farmers has increased (Kipkurgat, Onyiego, & Chemwaina, 2016).This disparity leads to service gaps; many smallholders lack access to reliable information to inform their decision-making and improve their livelihoods (FAO, 2015; Misaki et al., 2018; Ouma & Mann, 2021). With traditional extension services struggling to fill the knowledge gap and drive structural change, technology innovators and policymakers have increasingly turned to information and communication technologies (ICTs) to enhance information dissemination and market-making activities, particularly for the rural, inaccessible areas that are most often represented among agricultural livelihoods.

ICT for Agriculture in Kenya

While historically growth in the Kenyan agricultural sector was linked with investment in physical infrastructure (Wangu, 2014), ICTs and the emerging digital agriculture industry are now considered key factors in the present and future development of Kenya’s agricultural sector (van Schalkwyk, Young, & Verhulst, 2017). There is a growing interest among businesses and governments to integrate ICTs into their national agriculture strategies (FAO, 2015). The key role of ICTs in the agricultural context (ICT4Ag) is bridging information gaps in agricultural value chains, improving production via technical advisory services, increasing resilience (Hanson & Heeks, 2020), and increasing income through improved market linkages, price information, and access to financial services (FAO, 2015).

The past 15 years have seen the development of mobile-phone-based agriculture services—and later internet-enabled services—aiming to offer solutions to the various challenges within the Kenyan agricultural sector (Henze & Ulrichs, 2016) and to improve the quality and quantity of information flow (Emeana, Trenchard, & Dehnen-Schmutz, 2020; Misaki et al., 2018). As a result, a new mobile and digital agriculture industry has arisen (Kieti et al., 2021), populated by Kenyan and foreign tech startups, and national and global mobile service providers.

Mobile agriculture

Mobile-enabled ICT4Ag services emerged with increasing mobile phone adoption in the developing world. These services were brought to large groups of previously remote and disconnected people, including rural agriculturalists. There is a dearth of empirical evidence regarding the true impact of mobile agriculture services on farmers in developing countries. Even studies that assess the same mobile service often come to different conclusions, and existing research suffers from several methodological limitations (Baumüller, 2018), including relying on industry data that over-exaggerates successes by focusing on the limited number of farmers currently using the platform and not on the large number of farmers who are not (Ouma & Mann, 2021).

As a result, conclusive academic and scientific studies proving the value and impact of mobile agriculture are few, though still notable and generally positive. In some cases these studies affirm that mobile agriculture interventions were beneficial to small-scale farmers (Misaki et al., 2018), leading to greater savings, increased production, increased household income (Marwa et al., 2020), farmers’ confidence and trust, financial security, farm management, increased access to inputs, increased bargaining power, and social cohesion for smallholder farmers (Emeana, Trenchard, & Dehnen-Schmutz, 2020). The majority of studies between 2005 and 2015 examine best practices and planning for mobile-enabled agriculture interventions (Lubua, 2017), while others focus on impact, effectiveness, assessment of attitudes, empowerment and improved decision-making, and the potentialities of mobile technology for agriculture (Misaki et al., 2018).

The rise of internet-enabled devices and services

Early mobile agriculture services were limited to basic mobile phone functionality such as SMS and USSD. The ICT4Ag sector is, however, highly innovative, and changes in the availability of technology, such as increasingly affordable smartphones and tablets, continue to open up new possibilities (FAO, 2015). A migration is underway from cellular-enabled “mobile agriculture” to web 2.0 and internet-enabled “digital agriculture” services delivered to feature-phones, smartphones, tablets, and personal computers (Ezeomah & Duncombe, 2019). Internet-enabled services offer a far richer user experience than mobile-only services, as well as vastly increased interactivity and real-time interaction between service provider and user, and between users (Even & Nyathi, 2020).

While this is a global phenomenon, there has been a particular focus on Sub-Saharan Africa (SSA), which hosts 437 of the 713 digital agriculture services tracked globally by the global mobile network operators association (GSMA) in 2020. Kenya has by far the highest number of active digital agriculture services at 95—double that of Nigeria in second place (Phatty-Jobe, 2020). Kenya is also tied with Nigeria in having the continent’s highest number of digital agriculture startups (Kieti et al., 2021).

The transition towards internet-enabled services is illustrated by a 2017 assessment of e-Extension platforms in Kenya which found that 75% of users preferred accessing the platforms via internet-enabled devices (Gichamba, Wagacha, & Ochieng, 2017). A 2021 study found that approximately 34% of smallholder farmers own a smartphone (Krell et al., 2021), with 31% ownership for women and 38% ownership for men highlighting gendered accessibility constraints. Basic phones are owned by 56% of women compared to 48% of men (Krell et al., 2021), illustrating that a greater proportion of those transitioning from basic phones to smartphones are likely to be men.

It is worth distinguishing between ownership of and access to internet-enabled devices; not all who access internet-enabled digital agriculture platforms personally own the devices from which they access them. Sharing and borrowing of devices among households and communities, and posting on another’s behalf are common practices, and it has been estimated that as many as 40–45% of small-scale farmers in rural Kenya may already have direct or indirect access to the requisite technology to access internet-enabled services (David, 2020).

Smartphone ownership is generally indicative of higher income levels, as was the case for early basic phone adoption. The costs and barriers to basic phone adoption have, however, diminished over time so that they are now accessible even to most low-income households: 98% of Kenyans now own a phone (Krell et al., 2021). A similar trend is observable in smartphone adoption, as the cost of smartphones decreases over time and the value of smartphone ownership for improving livelihoods becomes more broadly demonstrated. For example, many “WhatsApp farmers” in Kenya liken buying a smartphone to investing in other infrastructure or tools to support their livelihood and the cost of data bundles to the cost of fuel, justified by the higher incomes generated through increased access to markets and information (David, 2020).

Digital agriculture

The perceived transformative potential of digital innovation for agriculture has resulted in substantial industry engagement devoted to exploring paths for data-driven agricultural development (Lazzolino, 2021). Digital platforms have greatly transformed the flow of information in agriculture, ensuring real-time communication and faster feedback for issues and best practices from the field and facilitating cross-learning and scaling up of innovations between projects and farmers (Even & Nyathi, 2020). Agricultural applications can promote productivity and performance of individual farmers, as well as that of whole agricultural value chains, supporting services, and connected sectors (Henze & Ulrichs, 2016).

Many digitally enabled agriculture services and platforms are designed to better connect producers and buyers and improve agricultural efficiency (Lazzolino, 2021), or offer small-scale growers new opportunities to engage in agriculture. Some providers target single or specific issues, while others offer complete platforms with multiple functionalities (Emeana, Trenchard, & Dehnen-Schmutz, 2020). Such platforms variously allow users to access higher-quality inputs such as seeds, fertilizer and advice; finance purchases and make payments; find laborers; negotiate with buyers; and make savings (Adelaja, 2021; Emeana, Trenchard, & Dehnen-Schmutz, 2020; Henze & Ulrichs, 2016). The GSMA subdivides digital agriculture platforms (DAPs) in SSA (n=437) according to: Digital Advisory Services (42%), Agri Financial Services (25%), Agri E-Commerce (16%), Digital Procurement (13%), and Smart Farming (4%) (Phatty-Jobe, 2020). The majority of digital agriculture platforms are led by telco operators, banks, agribusinesses, and governments/institutions (MercyCorps Agrifin, 2021a; Shrader, 2021; Shrader & Koyama, 2021). Globally, most digital agriculture platforms operate in only one country; under 25% operate regionally and only four operate on more than one continent. The user base of most platforms remains small. In 2020, less than a third had more than 100,000 users, and only 10% had over one million users (ISF Advisors, 2021).

Scaling and sustainability in digital agriculture

Digital platforms—which have come to dominate in other sectors—have lagged behind in agriculture (ISF Advisors, 2021), and there has been widespread speculation, research, and analysis aimed at understanding why this is the case. Until recently, the penetration and quality of digital connectivity among smallholder farmers was considered to be the primary constraint to adoption and scale of digital services. But, even as rural connectivity has improved, such platforms have gained little ground in agriculture (ISF Advisors, 2021). The historically fragmented mobile and digital agriculture ecosystem has been implicated in this dilemma (Kieti et al., 2021). Though many digital agriculture projects are created, many have been short-lived, disjointed, and financially unsustainable (Baumüller & Kah, 2019; Emeana, Trenchard, & Dehnen-Schmutz, 2020), with new entrants often trying to replicate the functionalities and business models of their predecessors (Mann, 2021). At present, all existing digital agriculture applications remain in the “pilot phase” (Ouma & Mann, 2021), Often after the pilot phase projects fail due to financial, human, and other constraints (FAO, 2015; Goedde et al., 2021). At times the blame for poor service performance has been directed towards end users, in this

case farmers, who are often older, more rural, poorer,, and less tech-literate than the typical technology adopter (Mann, 2021).

More recently, the blame for poor platform uptake has been directed towards the contextual constraints of smallholder-related agricultural markets. They are highly localized with volatile prices, low transaction values, localized/seasonal production, and typically cash-based transactions, taking place often in contexts that lack adequate physical infrastructure for efficient and widely networked exchanges (ISF Advisors, 2021). In other instances, limited adoption of mobile and digital agriculture services and platforms in rural agricultural communities has been attributed to mismatches between the design of these systems and end users’ literacy, skills, culture, and demands (Emeana, Trenchard, & Dehnen-Schmutz, 2020), and their perception of mobile phones primarily as devices for maintaining social networks rather than as tools for accessing agricultural information (Wyche & Steinfield, 2016).

The maintenance of such services also requires a consistent and unified approach by project initiators, service developers, funders/investors, implementers, researchers, internet providers, NGOs, policymakers, and agriculturalists (Emeana, Trenchard, & Dehnen-Schmutz, 2020). Studies rarely focus on describing the cooperative work among these actors that is required to make such services work locally, but this a crucial piece of the puzzle for understanding why some initiatives thrive where others fail (Christensen et al., 2019). The effectiveness of a rural e-service also depends on its design and delivery in accordance with the individual’s information needs, adaptive technologies, accessibility within a given infrastructure, affordable services with a rational business model, adequate awareness, and efficient communication with the respective community (Islam & Grönlund, 2010) (discussed in greater detail later in this review).

In recent years digital developers have begun to move towards integrated, consolidated platforms upon which individual apps can integrate and scale (Mann, 2021). This trend aligns with depictions of digital agriculture service users preferring a “one-stop-shop” for their agricultural activities (Kieti et al., 2021). These new bundled services often combine financial and nonfinancial services, offering saving and borrowing opportunities along with shared labor and expertise, joint purchasing of inputs and livestock, market aggregation, and access to shared storage facilities (Adelaja, 2021). By far the most successful digital agriculture platform of this type is Safaricom’s DigiFarm, which has more than 1.4 million registered users in Kenya (ISF Advisors, 2021; Mann, 2021).

It is worth acknowledging that a digital agriculture platform’s key assets, competencies, initial drivers, and core business mandate significantly shape the platform’s product offerings, sequencing, business model, and target customers (Shrader, 2021). This represents a top-down approach, which is prevalent among digital agriculture deployments. However, the focus of this literature review, and the broader research agenda that it supports, is on the horizontally integrated and/or bottom-up networking, communication, and collaboration afforded by social media/networking platforms, which are revolutionizing agricultural value chains in many ways.

Social platforms for agricultural extension

A majority of the literature on the intersection between social platforms and agriculture focuses on agricultural extension, most likely due to requirements for funding, monitoring, evaluation, and reporting. The “top-down” use of social media by agricultural extension offices for institutional agendas does not constitute the “true” definition of Social Agriculture, which is horizontal, user-to-user generated, and perpetuated without conventional institutional influence. Nonetheless, a brief discussion of social media for agricultural extension illuminates the rise of Social Agriculture and its role in filling gaps in traditional extension efforts.

Most traditional extension channels provide only a one-directional flow of broadly relevant information (Kanjina, 2021) that does not allow questions, clarification, in-depth training, or highly localized information. Social media’s interactivity can play a key role in new modes of dialogue in a broader context where knowledge is debated rather than merely transferred from advisors to farmers (Wims & Galvin, 2018). In-person farm visits by extension field agents provide an interactive channel whereby queries, clarification, or demonstration can be sought. However, government extension services in Kenya, as in many developing countries, have greatly decreased over the years (AgriLinks, 2017; Kioko, 2016; Wangu, 2014). Visits from extension officers are infrequent and brief—in 2014 the average farmer in Bungoma County had a mean of one extension visit per year (Gido et al., 2015)—and many field agents spend the majority of their time tackling the same perennial problems with each farmer (David, 2020).

The literature unanimously advocates for agricultural extension practitioners to adopt social media in their activities. In 2016, 95% of agricultural extension practitioners surveyed globally believed that social media can play an important role in bridging the gap between stakeholders (Bhattacharjee & Raj, 2016). At the same time, the literature broadly indicates that, despite the value proposition and positive perceptions of social media use for agricultural extension, this pathway is still somewhat underutilized in the agricultural extension sector (Bhattacharjee & Raj, 2016; Kanjina, 2021; Otene, Okwu, & Agene, 2018; Saravanan et al., 2018; Trendov, Varas, & Zeng, 2019). Uptake and interactive use of social media are often more advanced among farmers than among extensionists, academics, and researchers, who more often tend to use the platforms for one-directional messaging (Phillips, 2015, cited in Bhattacharjee & Raj, 2016).

A greater proportion of the literature identifies Facebook as the most popular or most widely used social media platform among agricultural extensionists (Akilu-Barau & Islam-Afrad 2017; Otene, Okwu, & Agene, 2018; Paudel & Baral, 2018), including the GFRAS global study (Bhattacharjee & Raj, 2016). Others indicate a preference for WhatsApp, notably those in India (AgriLinks, 2017; Dharmawan et al., 2020; Singh et al., 2019; Singh Nain, Singh and Mishra, 2019), or otherwise focus on WhatsApp (Thakur & Chander, 2018) in the study or report. What is clear from the literature on the use of social media for agricultural extension is its value in reaching and supporting vastly more clients via social media than is possible with in-person farm visits (AgriLinks, 2017; Bhattacharjee & Raj, 2016; Singh et al., 2021; Singh Nain, Singh & Mishra, 2019; Xinhuanet, 2018).

Despite the increasing adoption of social platforms among extension agents enabling them to serve larger networks of clients, they are still in high demand and are sometimes still not readily available to support their clients. As a result, many farmers seek alternative avenues for agricultural support and now have have diverse sources of agricultural information aside from extension services, including self-directed use of the internet and social platforms as sources of information (Kipkurgat, Onyiego, & Chemwaina, 2016), as well as platforms via which to communicate with other farmers and organizations (Kioko, 2016).

Social Agriculture

Rural smallholder agriculturalists are increasingly turning to social platforms as digital enhancement tools to improve their livelihoods (CTA, 2019). Social media platforms (such as Facebook, Instagram, Twitter, and YouTube) and social networking platforms (such as Facebook Messenger, WhatsApp, and Telegram) are significantly contributing to the digitization of agriculture both globally and in Kenya—arguably even more so than purpose-built digital agriculture platforms ever have. In comparison to digital agriculture platforms, social platforms are widely known and used for personal purposes, easily accessible and familiar, require no special training aside from that likely to be available within the community, and work on most models of smartphone regardless of brand or service provider (Devan & Kamala, 2018). Agriculturalists tend to prefer to use social media and messaging platforms with which they are already familiar and which are free to use instead of engaging with new channels (ISF Advisors, 2021).

A range of functionalities and affordances offered by social platforms has been appropriated by agriculturalists to serve their needs and support their livelihoods: sharing and accessing agricultural information, seeking markets for agricultural inputs and outputs, and mutually supporting the agricultural community to thrive. Such affordances include widespread networking; instantaneous and highly interactive communication between parties including large groups and audiences; smooth sharing and discussion interfaces; rich media user experiences including photo, video, audio, and text content;and the ability to create topic-specific or special interest pages and groups.

Social platforms, however, are not developed with agriculture in mind, and instead facilitate user-to-user communication and connectivity, the sharing of experiences and information via user-generated content, and the consumption of and interaction with this content. And yet, many of the ways that social media and networking platforms are being used for agricultural livelihoods mirror the intended use cases and value propositions of many purpose-built digital agriculture services and platforms—but typically in a much more organic, grassroots, horizontal, or bottom-up way.

Social platforms’ value proposition in agriculture

Many of the proposed and demonstrated use cases for social agriculture—the application of social platforms in agricultural value chains—reflect many of the value propositions among digital agriculture platforms more broadly, albeit sometimes via somewhat different means.

Provision of better access to information. The literature unanimously highlights the affordances granted by social platforms for accessing and sharing agricultural information. Advice and support on practices, crop varieties, inputs, solutions, risk management, etc., are sought and shared by fellow farmers, extension agents, agronomists, and other agricultural stakeholders using social platforms ( Akilu-Barau & Islam-Afrad 2017; Bhattacharjee & Raj, 2016; Bwalya, 2021; Kioko, 2016; Kipkurgat, Onyiego, & Chemwaina, 2016; Lohento & Ajilore, 2015; Maina, 2019; Mamgain, Joshi, & Chauhan, 2020; Nakhaye-Chesoli, Mwende-Mutiso, & Wamalwa, 2020; Paudel & Baral, 2018; Singh et al., 2021; Trendov, Varas, & Zeng, 2019; Wangu, 2014; Xinhuanet, 2018). Open access to information and easier content availability enable stakeholders to act as information brokers and innovators (Bhattacharjee & Raj, 2016). |

Provision of better connections with markets and distribution networks. Improved links among producers, suppliers and buyers that facilitate the formation of markets and networks (Paudel & Baral, 2018) can enhance value chains. Sellers can access market information (Kioko, 2016; Kipkurgat, Onyiego & Chemwaina, 2016; Lohento & Ajilore, 2015; Singh et al., 2021) and connect directly with customers (Bhattacharjee & Raj, 2016; Kipkurgat, Onyiego, & Chemwaina, 2016; Lohento & Ajilore, 2015; Trendov, Varas, & Zeng, 2019; Wangu, 2014; Xinhuanet, 2018), which can support direct and tailored marketing and sales, and circumnavigate brokers and middlemen (David, 2020; Xinhuanet, 2018). |

Empowerment of individual agriculturalists and rural communities. Social media can facilitate agricultural networking (Bhattacharjee & Raj, 2016; Kipkurgat, Onyiego, & Chemwaina, 2016; Thakur & Chander, 2018; Wangu, 2014) and strengthen links between farmers, extension workers, and researchers (Paudel & Baral, 2018) in such a way that farmer experimentation contributes to research agendas (Singh Nain, Singh, & Mishra, 2019) and facilitates the development of networks with other like-minded agricultural professionals (Mamgain, Joshi, & Chauhan, 2020; Paudel & Baral, 2018). Participatory interactions among stakeholders can innovatively use social platforms in the promotion of intervention (Nakhaye-Chesoli, Mwende-Mutiso, & Wamalwa, 2020) and ensure ongoing development and sustainability of projects (Singh Nain, Singh, & Mishra, 2019). Stories of success and failure help users to learn from others’ experience and build emotional bonds between users with shared experiences, and awareness created through social media can motivate and mobilize users to take action (Bhattacharjee & Raj, 2016). Social media use permeates different agricultural socioeconomic boundaries (Bwalya, 2021) and geographical boundaries (Mamgain, Joshi, & Chauhan, 2020; Paudel & Baral, 2018), allowing information to navigate and flow through diverse agricultural blocks (Bwalya, 2021). The horizontal and participatory structure of social platforms allows for an online community to develop and thrive as a group (David, 2020). There is value creation of knowledge to users and heightened potential for collaboration, driving the generation of social capital (Bhattacharjee & Raj, 2016). |

Time and cost savings. Farmers’ use of social media translates to reducing the time and cost for obtaining relevant and useful agricultural information (Thakur & Chander, 2018; Wangu, 2014; Bwalya, 2021). The immediate nature of social media communication helps users to receive timely advice or support (Bhattacharjee & Raj, 2016; Maina, 2019; Singh Nain, Singh, & Mishra, 2019; Thakur & Chander, 2018; Xinhuanet, 2018), which can improve efficiency and reduce losses in market-making activities, particularly for perishable produce, prevent crop and livestock losses during a pest or disease outbreak (Thakur & Chander, 2018), and enable rapid dissemination of crisis or emergency information and response strategies (Bhattacharjee & Raj, 2016). |

Low cost pathway for engagement and information. In comparison to other more traditional means, social platforms are a cost-effective means of spreading the word, getting support, and building professional and commercial networks among smallholder farmers and other rural agriculturalists (Akilu-Barau & Islam-Afrad 2017; Bwalya, 2021; Devan & Kamala, 2018; Ifejika et al. 2019; Raj & Bhattacharjee, 2013; Trendov, Varas, & Zeng, 2019; Wangu, 2014; Wims & Galvin, 2018). |

Highly interactive. One of the most notable parts of social platforms compared to many digital agriculture platforms is the level of interactivity afforded by social platforms, which is key to the value they drive (Bhattacharjee & Raj, 2016; Kanjina, 2021; Lohento & Ajilore, 2015). Social media allows for the creation of user-generated content, multi-directional interaction (Wangu, 2014), and complex and iterative sharing of information about lives and experiences (Andres & Woodard, 2013). Special interest groups, pages, subscriptions, hashtags, algorithms, etc. all enable filtering and sharing of common interests with others. Global content can be modified to local contexts; local content can have global context (Bhattacharjee & Raj, 2016). Anyone can share and receive information. There is value creation of knowledge to users, heightened potential for collaboration (Bhattacharjee & Raj, 2016), and the horizontal and participatory structure of social platforms allows for an online community to develop and thrive (David, 2020). |

Rich media experience. Social media affords the sharing and consumption of rich media, including photos, videos, audio, and text, all of which are widely utilized for agricultural applications and are perceived to greatly enhance the overall experience and value derived by users (AgriLinks, 2017; Bhattacharjee & Raj, 2016; Devan & Kamala, 2018; Ifejika et al. 2019; Kipkurgat, Onyiego, & Chemwaina, 2016; Mamgain, Joshi, & Chauhan, 2020;Paudel & Baral, 2018; Sebotsa, Nkurumwa, & Kyule, 2020; Thakur & Chander, 2018; Wangu, 2014; Xinhuanet, 2018). |

The majority of the literature focuses on the “institutional” context for social media use in agriculture. There are far fewer published studies that focus specifically on the “user-to-user” grassroots context that most accurately reflects the concept ofSocial Agriculture. Nonetheless, some of the literature sheds light on user experiences and preferences in relation to the use of social media for agricultural livelihoods.

The literature generally identifies Facebook and WhatsApp as by far the most prominent and popular social platforms used for agricultural purposes. Indeed, they are the two most commonly used digital social platforms in the world. The majority of those practicing Social Agriculture are likely to use multiple platforms in tandem. The flow may follow the pattern of broadcasting/wide-audience engagement via more open social media platforms (e.g., Facebook) and then following up, specializing, and closing deals via more closed social networking platforms (e.g., WhatsApp). Indeed, many agriculturalists often initially learn about certain WhatsApp groups via Facebook and then seek to join the group if it is relevant (David, 2020).

Case study: Facebook

In the literature centered on Kenya, Facebook typically prevails by a small margin in terms of popularity and prevalence of use for agriculture. Most studies focus on the seeking of agricultural information; a study in Kiambu County found that 42.9% of respondents use Facebook as their main social media platform when looking for agricultural information (Wangu, 2014). This figure is 47.3% in Njoro Subcounty (Sebotsa, Nkurumwa, & Kyule, 2020); Facebook is also the most common (personal) social media platform among farmers in Kesses District (Kipkurgat, Onyiego & Chemwaina, 2016).

A handful of gray literature publications highlight the numerous and diverse farming- and agriculture-related Facebook groups that already exist. The sheer number of groups present and their often large memberships—with many groups boasting tens to hundreds of thousands of members—are generally cited as proof of the success of these projects (Barth, 2019; BiznaKenya, 2019; Cole, 2019; Trendov, Varas, & Zeng, 2019; Wills, 2018). Many Facebook group leaders run groups as a labor of love and are neither paid nor trained. (Nearly 86% said the skills they used as community managers were self-taught.) These groups seek to create spaces in which members can connect and be supported by feelings of belonging, intimacy, and trust (TheGovLab, 2020). In 2018, 92% of the members of Africa Farmers Club (AFC, +100,000 members) who were actively practicing farming claimed that the group influenced the way they farmed and boosted their confidence. The majority of results stem from community knowledge sharing and a willingness to share knowledge freely, the emotional and community support sought and granted within the group, and the building of community that honestly and effectively enables farmers to help each other (Wills, 2018). A comprehensive Social Agriculture Ecosystem Report was produced to support the research, which discusses the prevalence and importance of agricultural groups on social media.

While the majority of published studies focus on the seeking and sharing of agricultural information via social platforms—indeed, this is a large part of the picture—much of social agriculture is in commerce and market-making and the affordances that social platforms grant for connecting sellers and buyers. Facebook has helped bridge the gap between buyer and seller, connecting them spontaneously and enabling quick closure of deals (BiznaKenya, 2019). In markets like Kenya, agricultural buying and selling patterns have been increasingly moving towards social platforms like Facebook. In 2016, Facebook was by far the most popular online forum for buying and selling produce in Kenya, outstripping the levels of activity on existing agriculture marketplace platforms by a factor of 30. The reasons for this success include that it is free to post, people are familiar with how to use it, and many people already have an account. Importantly, large farming Facebook groups have emerged, which provide a ready audience for buying and selling posts. In Kenya, there is a strong trend towards fruit and vegetables in digital selling patterns, likely because they are high value, perishable produce that is sold through a very unstructured value chain better suited to the informal structures of social media (Wills & Barrie, 2016). The intersection of social agriculture and social commerce discussed in greater detail later in this review.

Despite the prominence of Facebook in the literature, a 2020 study in Kenya found that, among the randomly selected baseline/control group (intended to be representative of the typical population in the rural Kenyan study area), only 5% were users of Facebook for agriculture, while 15% were users of WhatsApp for agriculture (David, 2020).

Case study: WhatsApp

In Kenya, an estimated 92–97% of smartphone owners use WhatsApp (David, 2020; Peterson, 2020), which has become intertwined with many aspects of business and personal life (Vogt, 2020). However, only an estimated 33% of smartphone users in rural areas—or 15% of the baseline population—use WhatsApp explicitly for agricultural livelihoods (David, 2020).

In 2015 the Technical Center for Agriculture and Rural Cooperation (CTA) noted that “literate young farmers and agripreneurs” were increasingly using WhatsApp as a platform for networking and exchange (Lohento & Ajilore, 2015). A 2020 study in Kenya found that 41.3% of participants used WhatsApp for agricultural information (Sebotsa, Nkurumwa, & Kyule, 2020). Interestingly, this study found that the use of WhatsApp in agriculture has a statistically significant positive effect on youth participation in agriculture, increasing it by 26.5%, speculated to be due to the affordance of rich media and immediate communication with professionals, mentors, and peers in agriculture.

Unlike Facebook—where anybody can search for, find, and join “public” groups—the closed nature of WhatsApp groups makes it harder to find data on their prevalence. Nonetheless, a selection of gray literature cites examples of WhatsApp use for agriculture, almost exclusively in relation to the group chat function (De Vries, 2016; FarmBizAfrica, 2017; Kioko, 2016; Maina, 2019; Xinhuanet, 2018). If well-managed and well-resourced with a strong collection of members, these WhatsApp groups can attain significant value in social capital. Some oversubscribed groups have long waiting lists (David, 2020) and others are approached by external commercial business interests (Maina, 2019).

Kenyan “WhatsApp farmers” in one study unanimously reported that WhatsApp groups overwhelmingly benefit their livelihoods and practice, and nearly all (91.7%) reported that WhatsApp has directly led to an increase in their income and livelihood. This is achieved primarily through increased access to markets and market information, and better or new farming practices leading to increased production and/or reduced loss. These benefits are enhanced by the “virtual community of practice” formed within strong groups, in which all members can communally learn from and interact with each other’s questions and feedback (David, 2020).

Agricultural WhatsApp groups are very diverse; some serve broad needs, interests, and geographical areas, and others focus on a highly specific sector or geographical area (or both). More specific groups can emerge independently or out of these generalist groups. Groups with the highest level of satisfaction among members are those with established rules, strong administration, and diverse membership (specifically including experts). These groups are typically very interactive; 96% of members are either “highly active” or “somewhat active,” and only 3% identified as “passive viewers.” By staying up to date on discussion, members can learn of new skills and experiences before they need to solicit advice themselves, allowing the group as a whole to learn about something they may never have thought to ask. This enables some farmers to transition from a reactive to a proactive approach. The mutually supportive and reinforcing atmosphere in the groups, where members support each other nearly as much as they benefit themselves, suggests they serve a need greater than just direct information dissemination or market-making (David, 2020).

While WhatsApp groups can be valuable sources of information and support, much of commerce and direct sales also happen over the platform (Xinhuanet, 2018). Thirty-eight percent of “WhatsApp Farmers” in Kenya report typically finding a buyer within 24 hours (often within even just a few hours or minutes), and only 7% report it taking more than 72 hours. Being able to easily market products while remaining on the farm is an incredible benefit. Buyers will often travel directly to the farmer, reducing transport costs, and some sellers are able to identify buyers prior to harvest, ensuring that less produce is spoiled or lost due to time spent searching for a market (David, 2020).

Demographics of social agriculture users

Digital divides still exist due to differences in wealth, gender, age, and education. Social media use, and thereby any considerations for social agriculture, expresses many of the same issues. Many demographic considerations in developing countries are also highly interconnected and reinforcing. For example, men are more likely to be better educated and to have greater social and financial power and autonomy, which is likely to drive other demographic factors, including wealth and access to technology.

Wealth Sufficient wealth with which to purchase an internet-enabled device is obviously a major factor in social media. Likewise, the cost of data is a consideration, especially considering that 99% of Kenya’s internet subscriptions are mobile-based. The literature almost unanimously points to higher wealth as a positive predictive indicator for digital inclusion generally (ICTWorks, 2020; Krell et al., 2021; Ouma & Mann, 2021), and wealth is often positively correlated with social media awareness (Adejo & Opeyemi, 2019). Smartphone ownership is significantly related to mobile agriculture service use (Krell et al., 2021). Ownership alone has been associated with increased access to mobile agriculture services; smartphone owners are twice as likely to use mobile agriculture services, even if the service is not internet-enabled and therefore doesn’t necessitate a smartphone for access and use (ICTWorks, 2020). Over a quarter of the baseline population in one Kenyan study reported being unable to afford a smartphone as the primary reason why they do not own one. However, cost is not the only barrier to access; personal choice, reticence, and/or technological literacy are also significant factors (David, 2020). |

Education Level of education is one of the strongest indicators for the use of mobile/digital agriculture services and social media. Farmers who completed primary school or at least some secondary school were three to four times more likely to use mobile agriculture services (ICTWorks, 2020). The same trend is true of social media awareness and use, both personally and for agricultural livelihoods (Adejo & Opeyemi, 2019; David, 2020; Kimani, Nyang’anga, & Mburu, 2019; Omotoso-Ajayi, 2015). Level of education is highly correlated with level of social media familiarity; in one study in Kenya, 75% of farmers with postsecondary education had a thorough knowledge of social media compared to 18% of those with secondary education and 9% of those with primary education. Correspondingly, all the farmers entirely lacking formal education had never heard of social media (Kimani, Nyang’anga, & Mburu, 2019). Among “WhatsApp farmers” in Kenya, 90% had postsecondary education compared to the baseline/control group, of which only 15% had the same, indicating a highly significant bias of WhatsApp group participation towards the most educated farmers (David, 2020). In Nigeria, a similar positive relationship has been observed between level of education and both the level of social media usage (Adejo & Opeyemi, 2019) and use-intensity by agro-entrepreneurs (Omotoso-Ajayi, 2015). |

Location and housing A 2019 study on social media familiarity among smallholder farmers in Kenya found no significant association between social media awareness and location in urban, peri-urban, and rural areas. This means that farmers in the target area were found to be more or less similar in terms of social media awareness irrespective of where they came from (Kimani, Nyang’anga, & Mburu, 2019). A study in Nigeria found that household size was positively correlated with the probability of social media usage (Adejo & Opeyemi, 2019), which may reflect the prevalence of sharing or borrowing internet-enabled devices within families and communities (David, 2020). |

Gender Literature on the digital divide indicates a considerable bias towards men compared to women, and the literature on social media and agriculture broadly confirms this. While much of the literature in academic and government spheres stresses the importance of age, location, and education in defining the digital gender gap, other significant factors have been identified, including participation in farmer organizations (within which women are underrepresented) and smartphone ownership (Krell et al., 2021). Women in low-income countries are 8% less likely than men to own a basic mobile phone and 20% less likely to use mobile internet services than men. The gap is even more pronounced in Sub-Saharan Africa and South Asia, where women are 37% and 51% less likely, respectively, to use mobile internet services (ISF Advisors, 2021). In Kenyan smallholder communities, women were less likely to use mobile agriculture services in comparison to men (Krell et al., 2021), with men 1.2 to 1.35 times more likely than women to use mobile agriculture services (ICTWorks, 2020). Women in Kenya are less likely than men to own an internet-enabled phone; 31% of women in Kenya own a smartphone compared to 38% of men, and basic phones are owned by 56% of women compared to 48% of men (Krell et al., 2021), illustrating that a greater proportion of those transitioning from basic phones to smartphones are likely to be men. Kenyan men are “better versed” with social media in general than women (Kimani, Nyang’anga, and Mburu, 2019), and the majority of “WhatsApp farmers” in Kenya are men (71.7%), despite women representing 80% of the baseline population of the communities practicing agricultural livelihoods included in the study (David, 2020). These trends not only affect women’s individual and collective ability to benefit from social agriculture and other technological innovations, but also impact the representation of women’s voices and experiences in the shaping of social agriculture. However, social-media-enabled informal social commerce is particularly popular among women entrepreneurs, who are vastly overrepresented in the space, particularly in contexts where social norms mean that women are expected to manage household duties alongside their business activities and/or may be financially excluded and unlikely to get community or institutional support to start a formal business or attract investment (Roest & Bin-Humam, 2021a, 2021b) |

Age Younger farmers have been found to be more familiar with social media compared to older farmers (Kimani, Nyang’anga, & Mburu, 2019), and increased age among research participants is negatively correlated with level of social media usage (Adejo & Opeyemi, 2019). “WhatsApp farmers” in Kenya tend to be younger than the baseline population average by approximately five years, with an average age of 35.2 years (David, 2020). The majority of WhatsApp produce sellers in an Indonesian market are millennial-aged (Akhmadi et al., 2021). Interestingly, a 2020 study on the use of mobile-enabled agricultural services found that age is not significantly related to use of (traditional) mobile agriculture services (ICTWorks, 2020), suggesting that the deciding factor may be related to social media or the inclusion of internet connectivity in general. This trend bodes well for greater age-based inclusion as internet-enabled device access and ownership continue to grow in the region. |

Youth in social agriculture

Unsurprisingly, the literature broadly indicates that both social media use in general and social media use for agricultural livelihoods specifically are more prevalent among youth; social agriculture users tend to be younger on average than the general population. However, in recent decades Kenyan agricultural livelihoods have largely been characterized by older demographics, as many youth have tended to harbor negative perceptions towards agricultural livelihoods (Adedugbe, 2014; Geza et al., 2021; Irungu, Mbugua, & Muia 2015; Lohento & Ajilore, 2015; Maslin-Nir 2019), and increasingly abandon agriculture to migrate to urban areas to look for alternative opportunities (Henze & Ulrichs, 2016). This trend has been broadly documented worldwide (USAID, 2019).

The average farmer’s age in Kenya today is 60 years (Henze & Ulrichs, 2016) and only 20% of farmers fall in the youth category of 18 to 35 years (Kimani, Nyang’anga, & Mburu, 2019). This pattern is broadly applicable to the African continent, where about 60% of the population is under 24, while the average farmer’s age is 60 (FAO 2014, cited in Maslin-Nir, 2019), raising concerns of lacking farmers to replace Africa’s current generation when they die (Maslin-Nir, 2019). Simultaneously, the youth represent 37% of the Kenyan population, but constitute more than 70% of the unemployed (IEA, 2016, cited in Henze & Ulrichs, 2016).

With these factors in mind, the reviewed literature broadly advocates for reengaging the youth with agriculture through digital agriculture and social platforms to help tackle youth unemployment and an aging farmer population. Likewise, the literature typically identifies that youth attitudes and perceptions towards agriculture are shifting in a positive direction; the inclusion of digital solutions is widely cited as the leading cause of this shift. Through social media, modern agricultural livelihoods are becoming more attractive to youth (Lohento & Ajilore, 2015) and are increasingly seen as viable and profitable business opportunities (USAID, 2019) quite different from the subsistence agriculture of the past. Today’s agriculture requires digital skills to increase productivity, solve challenges (USAID, 2019), find niche markets and ventures, and adopt innovations and modern agricultural technologies (Wangu, 2014). Technologically enabled farming can be skillful, rewarding, profitable, and not necessarily labor-intensive (Lazzolino, 2021). African governments and media alike are intentionally cultivating this image , encouraging younger generations into agriculture to ensure the future viability of the sector (Lohento & Ajilore, 2015; Maslin-Nir, 2019). Activists on social media have begun to take on the challenge of shifting perceptions of agriculture in order to address food shortages (USAID, 2019).

In 2013 the International Institute for Communication and Development (IICD) reported that more young people in Western Kenya had shown an interest in investing in farming, linking that trend to the recent inclusion of ICT in farming, which 90% of the 24-38-year-old farmers in the study were using (Plechowski, 2014). This is confirmed by recent literature that directly assesses age among digital agriculture and social social media platform users (Adejo & Opeyemi, 2019; David, 2020; Kimani, Nyang’anga, & Mburu, 2019). A 2020 study on youth participation in agriculture in Njoro Subcounty, Kenya, found that the level of social media platform use has a significant effect on youth participation in agriculture—notably WhatsApp use, which was shown to increase youth participation in agriculture by 26.5% (Sebotsa, Nkurumwa, & Kyule, 2020). Young agriculturalists supported via ICT to improve production and farm management not only increased their incomes but they also gained respect and social status in their communities (FAO, 2015). A 2020 scoping review on youth participation in agriculture found that the key challenges are centered around knowledge availability, production resources, and lack of infrastructure, support, and access to advisory services (Geza et al., 2021). Many of these challenges can be met or supplemented via social platforms, where youth can ask questions about how to start agribusiness, receive ongoing community support throughout their ventures, and ultimately contribute to the shared knowledge and experience base themselves (Adedugbe, 2014). The majority of young social agriculturalists own smartphones and extensively use social media to research and discuss their produce and production methods, follow market and farming trends, respond to queries from customers or fellow digital farmers, advertise their products, and make sales (Lazzolino, 2021).

Social commerce in social agriculture

Within the literature on the intersection between social platforms and agriculture, there is considerably more focus on information pathways than there is on commerce. The explicit intersection of social commerce with agriculture is broadly lacking in the literature. Yet social commerce is a key part of social agriculture, in which transactions may involve agricultural inputs and outputs, or (both practical and consultational) services and information. Social commerce as a field of its own has been widely studied, both theoretically and practically, and there exists a wealth of literature on it from which we can draw to illuminate the discussion of social agriculture. There is a relatively small (but growing) body of literature on truly informal user-to-user social commerce in emerging markets.

Social media platforms have become significant pathways for both formal and informal e-commerce. Aside from use for formal commerce and monetization, social platforms have become powerful tools for informal user-to-user commerce or “informal social commerce”—in which goods are bought and sold via social platforms entirely without a trusted third party facilitating transactions. Formal e-commerce platforms offer end-to-end mediation of the buyer-seller interaction, including matching supply and demand, facilitating and securing payments, and fulfilling orders and dispatch. In social commerce, supply and demand are illustrated—and buyers and sellers connected—solely via social platforms, which do not necessarily engage directly in other aspects of online commerce and do not generally accommodate payments or delivery services. Consequently, those steps happen off-platform in whatever configuration works for the buyer and seller based on their circumstances—often fragmented and highly situational (Islam & Roest, 2020).

Theoretical frameworks for social commerce

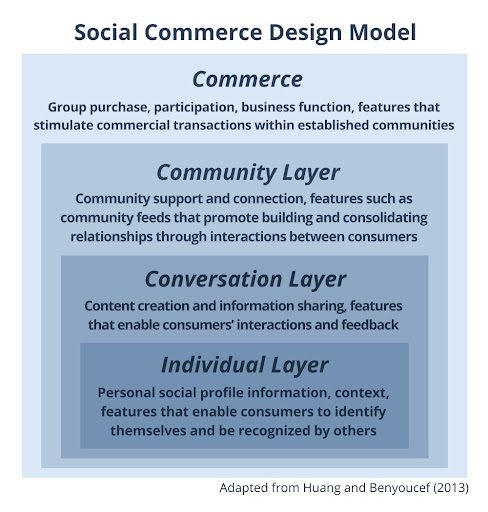

A 2018 study on the interaction of trust and social influence in social commerce identified a range of key factors involved in social commerce: Consumer Satisfaction, Trust, Communication, Information Quality, Reputation, Transaction Safety, and Word of Mouth (Beyari & Abareshi, 2019). Huang and Benyoucef (2013) proposed that the social commerce design model consists of four interconnected layers that constitute the building blocks of a social commerce platform (top right).

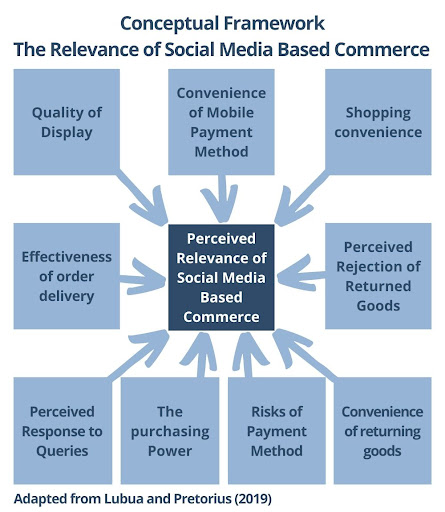

A 2019 study on social commerce in the African context (Lubua & Pretorius, 2019) developed a conceptual framework by which to determine the relevance of social-media-based commerce to social media users (bottom right). It is important to consider that each of these factors will be assessed by comparison to the next best alternative within the sphere of interaction. In areas where alternatives are scarce, such as emerging markets, social commerce is likely to be more relevant.

Social commerce in emerging markets

Truly informal social commerce, also called “chat commerce” (Chuwiruch, 2021), is particularly prevalent in emerging markets/developing countries (Camacho & Barrios, 2021; Gibreel, Al Otaibi, & Altmann, 2018; Lubua & Pretorius, 2019). In many countries where “traditional” e-commerce was not yet well established before the widespread adoption of mobile internet and social media, internet-based commerce is leapfrogging over conventional e-commerce straight to social commerce (Gibreel, Al Otaibi, & Altmann, 2018). Unlike more established e-marketplaces, social platforms aren’t generally designed for commerce and don’t include integrated payment systems, so customers need to use external payment methods (Chuwiruch, 2021), including mobile money (Islam & Roest, 2020). In many instances, particularly in emerging markets, this may in fact be part of the appeal of social commerce, particularly among users without traditional bank accounts with which to make formal e-commerce payments (Osano & Languitone 2016, cited in Lubua & Pretorius, 2019). Informal social commerce also typically involves minimal registration requirements, does not require a business license, and offers flexibility in payment methods by allowing sellers and buyers to use whatever methods are available to meet their respective needs (Kikulwe et al., 2014, cited in Lubua & Pretorius, 2019; Roest & Bin-Humam, 2021). It also requires little upfront investment (Roest & Bin-Humam, 2021), which may appeal to individuals less- or entirely un-integrated into traditional financial systems (Lubua & Pretorius, 2019).

Informal online commerce cuts across socioeconomic classes, and the flexibility and low barriers to entry make it particularly popular among women entrepreneurs, who are vastly overrepresented in the space – particularly in contexts where social norms mean that women are expected to manage household duties alongside their business activities, and/or may be financially excluded and unlikely to get community or institutional support to start a formal business or to attract investment (Roest & Bin-Humam, 2021a, b). Informal social commerce has also been credited with enabling buyers and sellers to circumvent middlemen and brokers (Gibreel, Al Otaibi, & Altmann, 2018), who often use their position to enhance their bargaining power and take advantage of sellers (David, 2020; Xinhuanet, 2018).

Informal social commerce has become especially popular in South and Southeast Asia, where many buyers also seem to prefer the social nature of the social commerce transaction to the impersonal and regimented e-commerce experience (Islam & Roest, 2020). Likewise, informal social commerce is seemingly popular in cultures where haggling and more personal interaction between buyers and sellers are the norm (Chuwiruch, 2021). For example, farmers in Zimbabwe turned to social media when the COVID-19 pandemic lockdown conditions halted their typical sales avenues. Buyers were also keen to use this new system as a lower-risk method of obtaining their produce, and family members of the diasporic population were noted to buy food via social media for their struggling family members in Zimbabwe (Mambondiyani, 2020). However, transitioning to online business does require learning new technical and business skills; a study on fresh produce sellers in Palembang, Indonesia, found that paid Instagram ads failed to enhance content engagement due to the inexpert management of social media advertising campaigns by sellers with low tech literacy (Wahid, 2021).

Social platform affordances for social commerce

Integrated payments and built-in affordances for social commerce via social media are currently being developed and introduced, namely by the Meta empire (including Facebook, WhatsApp, Instagram, discussed later). Facebook Marketplace is more closely aligned with social commerce, as the majority of listings are user-generated and transactions are typically user-to-user, with users handling payment and collection/delivery independently off-platform. However, many social commerce interactions on Facebook, especially within emerging markets and social agriculture, do not use the Marketplace feature but instead rely on posting and discussion in groups and via news feeds (Wills, 2018).

A range of other platform-based social and functional affordances have been identified and adopted—typically in organic, grassroots, and intuitive ways adapted to the needs of users—in the pursuit of social-media-based entrepreneurship and informal social commerce. Clearly there is far more to the picture than simply buying and selling. A 2020 study on the social commerce affordances of Facebook for female entrepreneurship documents practices that combine entrepreneurial-oriented actions with Facebook features in the pursuit of four entrepreneurial outcomes: identifying business opportunity, building a market, trust building, and value creation. The study identified eleven key affordances for truly informal social commerce and “digital subsistence entrepreneurship” (Camacho & Barrios, 2021).

Identifying Business Opportunity | Monitoring: Consumption and entrepreneurship are interwoven, business opportunities are informed by previous learning as consumers, and “consumer skills” are used entrepreneurially. Social networks become a source of market information. Seeing social media entrepreneurship motivates others to do the same. |

Building a Market Usually starts with close networks (e.g., family and friends), extends via loose connections (friends of friends) and beyond. | Profiling: Using searches and timeline to learn about the needs and behaviors of one’s network and to discover patterns to encourage business exchanges. |

Visibility: Using sharing features to access a larger audience, increase presence, reduce customer uncertainty, and enhance “electronic-word-of-mouth.” | |

Connection: Using searches, events, fan pages, and friend invites to grow one’s network, reach more potential customers, and leverage such connections for business. | |

Content association: Using searches, sharing, tagging feelings, or “liking” specific content to create an attractive business profile for potential and current customers. | |

Persistence: Using features to keep knowledge about the business available on the platform over time. | |

Trust Building | Generative role taking: Playing simultaneous, varied roles, such as friend, expert, or seller, to strengthen relationships and generate affinity and trust with customers. |

Community engagement: Using features such as comments, sharing, posting, events, likes, timelines, and fan pages to promote interactions within the community. | |

Customized engagement: Using features such as news feeds, posts, comments, and private messages to develop personalized relationships with one’s audiences. | |

Value Creation Strengthen marketplace literacy and complexity. | Supervising: Using notifications, likes, shares, and comments, as well as feelings/activities, to assess activities related to one’spage and products. |

Experimenting: Using features to develop fast cycle, low-cost, interactive studies assisting innovation, refinement of products, and evaluation of customer acceptance. |

Adapted from Camacho & Barrios (2021).

Trust in social commerce

Trust is one of the key barriers to the adoption of digital solutions (ISF Advisors, 2021). Aside from facilitating transactions, third-party intermediaries often play a role in facilitating trust: providing assurances and guarantees of product authenticity, providing secure payment pathways, or facilitating return policies in the case of buyer dissatisfaction. Other platform marketplaces “curate” the user base to build trust and prevent bad behavior, restricting who can join and/or what activities users can undertake, imposing user authentication, and/or closely monitoring user activity to avoid illegal or inappropriate behavior (ISF Advisors, 2021).

In the absence of a trusted third party, users of social platforms for informal social commerce must be inclined to develop trust and understand the inherent risk incurred on both sides of online interactions. Informal social commerce establishes trust built on social capital embodied in and interconnected with social networks and mediated by the community of the sellers and buyers themselves (Gibreel, Al Otaibi, & Altmann, 2018). Social capital is defined as “i) the good will, sympathy, and connections created by social interaction within and between social networks and ii) the value created by social relationships, with expected returns in the marketplace” (WordNik, n.d.).

The table above illustrates three practice-based affordances employed to build trust for informal social commerce. Trust is positively related to consumer satisfaction, communication, information quality, reputation, and word of mouth (Beyari & Abareshi, 2019). Private groups with exclusive or specific admission policies were also found to provide more trust assurances to participants than regular consumer-to-consumer platforms (e.g., eBay, Craigslist) (Moser et al., 2017, cited in Camacho & Barrios, 2021).

Future integration of social commerce functionality into social media platforms

Informal social commerce emerged long before any intentional affordances for it were purposely built into social platforms by their designers. Even today, unlike more established e-marketplaces, social media platforms aren’t designed for commerce and don’t include payment systems, necessitating customers to use external payment methods (Chuwiruch, 2021), including mobile money (Islam & Roest, 2020). However, in response to this and with appreciation of the huge amount of commerce being undertaken via social platforms, designers are beginning to integrate explicit social commerce functionalities into platform design. For example, WhatsApp (owned, along with Instagram, by Facebook) is introducing WhatsApp Pay, which will allow WhatsApp users to complete digital transactions without leaving the platform (Purohit & Bonnici, 2021; WhatsApp, 2021). They have also introduced the WhatsApp for Business API, which affords integration of business features into the typical WhatsApp functionality (Mercycorps Agrifin, 2021b; Peterson, 2020). These include “business profiles,” quick/automated replies, labels and categorization/organization of contacts and chats, listing of catalogs, and a “shopping-cart”-based ordering system (Peterson, 2020; WhatsApp, 2021).

The risks of platformization

The ubiquity of platforms such as WhatsApp and Facebook, and the level of integration they have achieved into the day-to-day functioning of many societies, has made them indispensable in the functioning of many lives and livelihoods. These platforms have become so crucial to global communications infrastructure that when they go down for technical reasons, entire countries, segments of national economies, and even some basic daily governmental activities nearly grind to a halt (Waldron, 2021). This was the case in the unprecedented global outage of all Facebook products (including WhatsApp and Instagram) at 15:39 UTC on October 4, 2021: “It was basically like the entire internet was out. That was the perception”(Waldron, 2021).