How many people have platform livelihoods in Indonesia?

There are many kinds of platform livelihoods—combinations of working, selling, renting, and creating. This makes it difficult to accurately count the number of people involved, particularly when individuals can a) use more than one platform, b) earn part time via a platform, and/or c) employ others to help them with their platform livelihood. There are several methods for enumeration: nationally representative surveys, analytic estimation, and (the approach used in this review) the aggregation of reports from individual platforms.

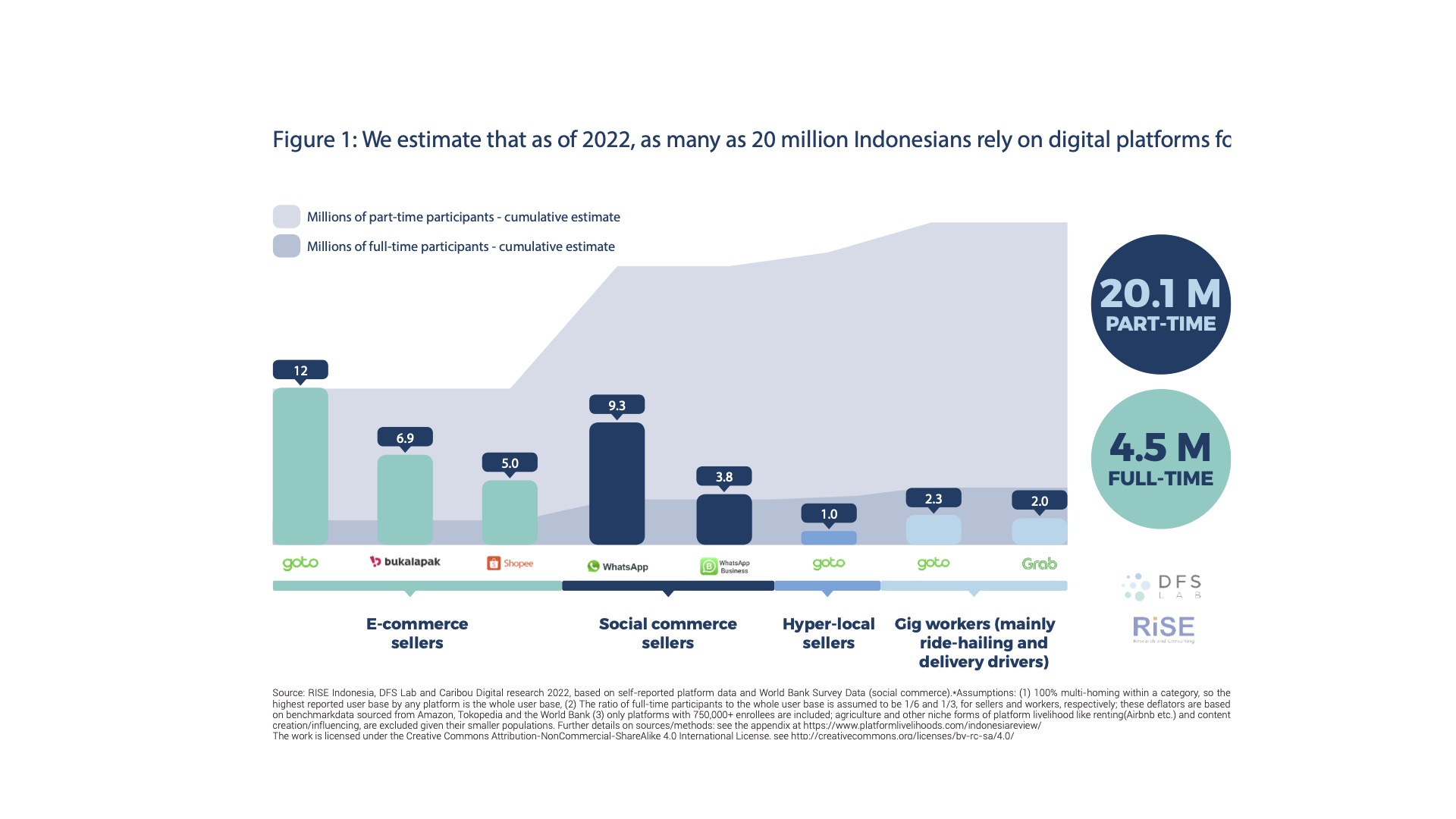

Evidence from a 2019 World Bank survey suggests at least 1.2 million Indonesians were involved in gig work, mostly in ride-hailing, transport, and logistics/delivery, and 13 million in varying degrees of e-commerce, particularly informal social commerce. More recent bottom-up figures from platforms are proportionally in alignment with these estimates, but they reflect a significant boost due to continued platform expansion and the pandemic.

Reports from the platforms do not distinguish between full time and part time workers and sellers. In gig work, we estimate at least 2.25 million active delivery drivers and ride-hailers. In trading, we identify 12 million e-commerce vendors, 9.3 million informal social commerce sellers, 1 million hyper-local merchants in food prep and rapid fulfillment, and 60,000 farmers and fishermen. These are four reasonably distinct, non-overlapping categories of engagement. In renting, we estimate 221,000 property owners, and in creating perhaps 7,000 high-visibility, high-earning creators.

These reports suggest that in 2022 as many as 20 million Indonesians earned at least some of their livelihood via online marketplaces and/or social platforms. Of these, as many as 4.5 million may do so exclusively. The exclusivity numbers are much smaller because many individuals have multiple sources of income and earn only fractionally from platform sources.

Nevertheless, a figure of 20 million represents approximately 1 in 5 of Indonesian workers. This degree of participation is clearly enough to merit continued attention from policymakers, technologists, and the digital development community.